¶ 1. Overview

The Bank Reconciliation feature allows law firms to reconcile their bank statements with the transactions recorded in LawPractica. This process ensures that:

- Bank balances match system balances

- All deposits and withdrawals are accounted for

- Errors, omissions, or duplicates are identified

- Trust and general accounts remain compliant and audit‑ready

Bank reconciliation is a mandatory accounting practice and is especially critical for trust accounting, where strict regulatory rules apply.

¶ 2. When to Use Bank Reconciliation

Bank reconciliation should be performed:

- Monthly (required for trust accounts)

- After receiving a bank statement

- After periods of high transaction volume

- Before audits or financial reviews

- When discrepancies appear in trust or general balances

This ensures accurate financial reporting and compliance with law society trust rules.

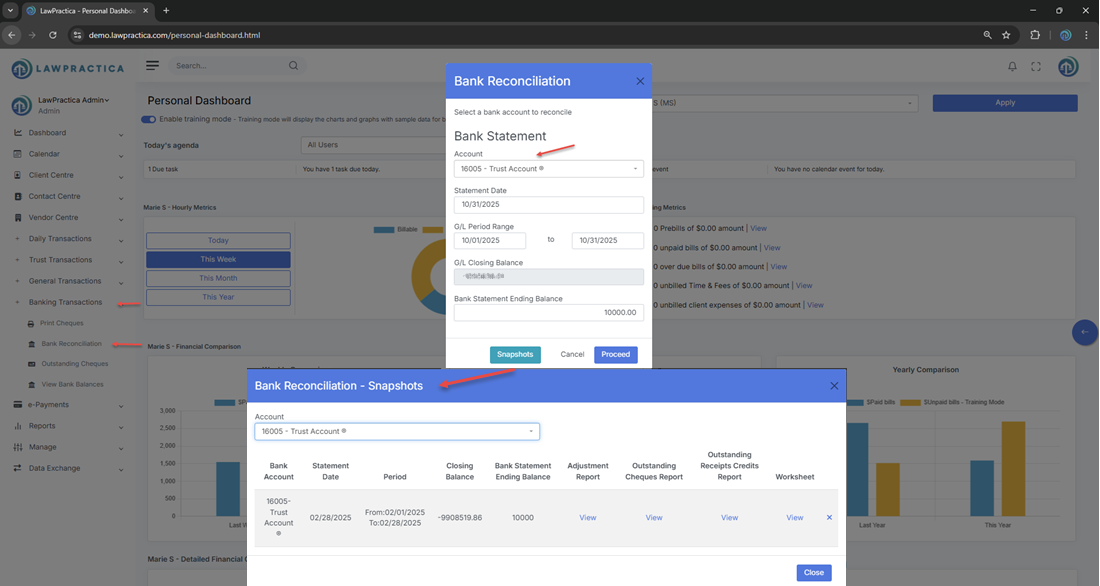

¶ 3. Selecting the Bank Account

- At the top of the reconciliation screen, users select the bank account they want to reconcile.

¶ Supported Accounts

- Trust bank accounts

- General (operating) bank accounts

- Additional firm bank accounts (if configured)

- Why It Matters

Each account has its own ledger and must be reconciled separately.

¶ 4. Entering Statement Information

Users must enter:

- Statement Date

- Statement Ending Balance

- Statement Opening Balance (if required)

This information is used to compare the bank’s reported balance with the system’s calculated balance.

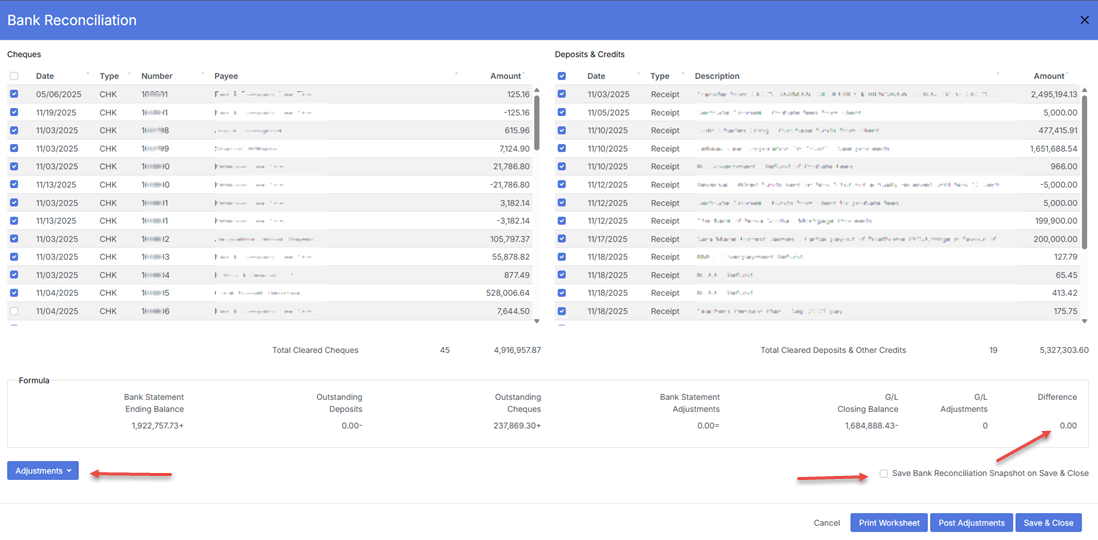

¶ 5. Matching Transactions

The reconciliation screen displays all uncleared transactions recorded in LawPractica, including:

¶ For Trust Accounts

- Trust Receipts

- Trust Cheques

- Trust Transfers

- Trust Transfer Cheques

¶ For General Accounts

- General Receipts

- General Cheques

- Journal Entries (bank‑related)

Users mark each transaction as Cleared once it appears on the bank statement.

¶ 6. Cleared vs. Uncleared Transactions

¶ Cleared Transactions

- These appear on the bank statement and are checked off during reconciliation.

¶ Uncleared Transactions

- These remain outstanding and may include:

- Cheques not yet cashed

- Deposits not yet processed

- Timing differences

- Errors requiring investigation

- Uncleared items carry forward to the next reconciliation period.

¶ 7. Adjustments & Corrections

If discrepancies exist, users may:

¶ Add Adjustments

- Bank charges

- Interest earned

- Service fees

- Corrections for rounding differences

¶ Investigate Errors

- Duplicate entries

- Missing transactions

- Incorrect amounts

- Wrong bank account selection

- All adjustments are logged for audit purposes.

¶ 8. Completing the Reconciliation

- The reconciliation is complete when:

- Statement Ending Balance=System Balance After Cleared Items

- Once balanced, users select Reconcile & Close.

¶ System Updates

- Locks the reconciliation period

- Generates reconciliation reports

- Updates trust and general audit logs

- Carries forward uncleared items

- Reconciliations cannot be edited after posting — they must be reversed and redone if corrections are needed.

¶ 9. Compliance Notes (Especially for Trust Accounts)

Trust accounting rules require:

¶ 1. Monthly Trust Reconciliation

- Mandatory for all trust accounts.

¶ 2. No Overdrafts

- Trust accounts must never show a negative balance.

¶ 3. Full Audit Trail

Reconciliation must record:

- Statement date

- Statement balance

- Cleared items

- Uncleared items

- Adjustments

- User who completed the reconciliation

¶ 4. Supporting Documentation

- Printed or exported reconciliation reports must be retained for audits.

¶ 5. Accuracy

- All trust transactions must be matched to bank activity.

- The Bank Reconciliation feature ensures firms meet these requirements.

¶ 10. Integration with Other Features

Bank Reconciliation integrates with:

- Trust Transactions – Trust receipts, cheques, transfers

- General Transactions – General receipts, cheques, journal entries

- Trust Ledger – Updates cleared/uncleared trust activity

- General Ledger – Updates cleared/uncleared general activity

- Reports – Trust reconciliation reports, bank summaries, audit logs

- Find – Investigate discrepancies and reverse transactions

This creates a complete and compliant financial ecosystem.

¶ 11. Summary

The Bank Reconciliation feature provides a structured, compliant method for reconciling bank statements with trust and general ledger activity. With support for cleared/uncleared matching, adjustments, audit logging, and trust‑accounting compliance, it ensures accurate financial management and regulatory readiness across the firm.