¶ 1. Overview

The Journal Entry feature allows law firms to create manual accounting entries that adjust balances in the general ledger. Journal entries are essential for:

- Correcting posting errors

- Adjusting balances

- Recording non‑cash transactions

- Year‑end accounting adjustments

- Reclassifying amounts between accounts

This feature ensures that all manual adjustments are properly documented, balanced, and included in financial reporting and audit trails.

¶ 2. When to Use a Journal Entry

Journal Entries are used when:

- A transaction was posted to the wrong general ledger account

- An accountant needs to adjust revenue, expense, asset, or liability balances

- A correction is required that cannot be made through standard workflows

- Non‑cash adjustments must be recorded (e.g., accruals, write‑downs)

- Reclassification between accounts is needed

- Year‑end adjustments are required

- Journal Entries must not be used for trust‑accounting corrections — those must be done through Trust Transfer or Trust Cheque.

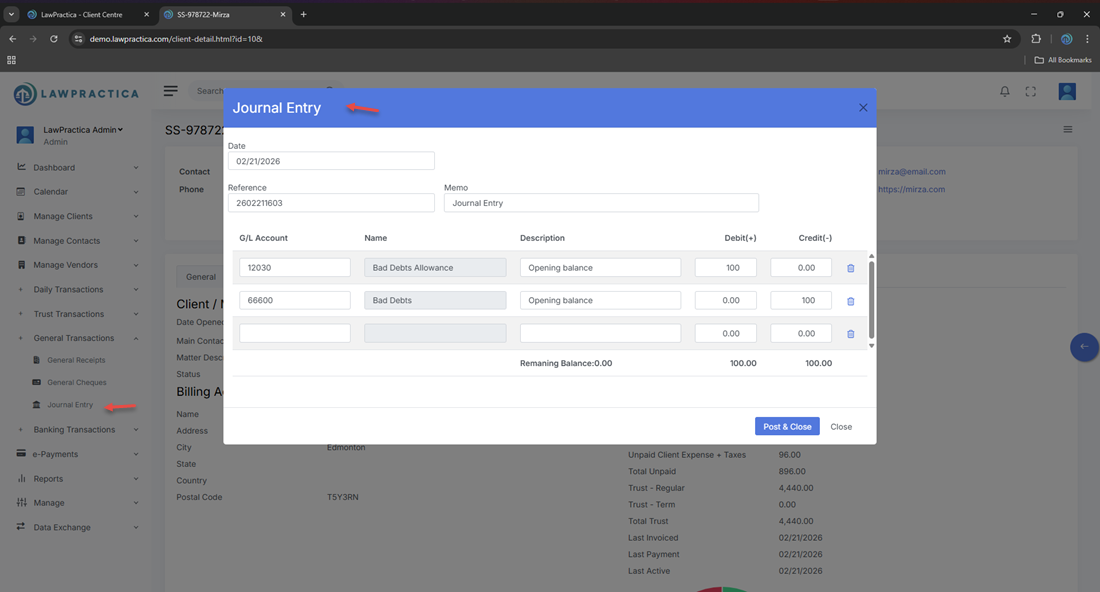

¶ 3. Debit & Credit Lines

A Journal Entry consists of two or more lines:

¶ Debit Line(s)

- Increases assets or expenses

- Decreases liabilities, equity, or revenue

¶ Credit Line(s)

- Increases liabilities, equity, or revenue

- Decreases assets or expenses

¶ Balancing Requirement

- The total debits must equal total credits before posting.

- The system will not allow posting unless the entry is balanced.

¶ 4. Account Selection

- Users must select the general ledger accounts affected by the adjustment.

¶ Account Types Include

- Bank accounts

- Revenue accounts

- Expense accounts

- Asset accounts

- Liability accounts

- Equity accounts

Selecting the correct accounts ensures accurate financial reporting.

¶ 5. Date & Reference Number

¶ Date

- The effective date of the adjustment (e.g., month‑end, correction date).

¶ Reference Number

- System‑generated or user‑entered for tracking and audit purposes.

¶ 6. Description / Memo

A clear description must be entered to explain the purpose of the journal entry.

¶ Examples

- “Correction: Payment posted to wrong expense account”

- “Year‑end accrual for unpaid vendor invoice”

- “Reclassification of prepaid expense”

- “Adjustment for bank reconciliation variance”

This description appears in all audit logs and financial reports.

¶ 7. Posting the Journal Entry

When the user selects Post & Close, the system:

¶ General Ledger Effects

- Updates all affected accounts

- Records the debit and credit entries

- Adjusts balances immediately

¶ Audit Trail

- Logs user, timestamp, accounts, and amounts

- Ensures compliance with accounting standards

- Journal Entries cannot be edited after posting — they must be reversed if corrections are needed.

¶ 8. Compliance Notes

Journal Entries must follow standard accounting rules:

¶ 1. Balanced Entries

- Debits must equal credits.

¶ 2. Full Documentation

Every entry must include:

- Date

- Accounts

- Amounts

- Description

- User who posted it

¶ 3. No Trust Adjustments

- Journal Entries cannot be used to adjust trust balances.

¶ 4. Audit Trail

- All entries must be traceable and reviewable.

¶ 5. Reconciliation

- Journal Entries must appear in:

- General ledger

- Financial statements

- Audit logs

¶ 9. Integration with Other Features

Journal Entry integrates with:

- General Ledger – Updates account balances

- Reports – Financial statements, trial balance, audit logs

- Find – Search and reverse journal entries

- General Cheque / General Receipt – Correcting misposted transactions

- Daily Activities – Supports billing‑related adjustments

This ensures a complete and accurate general‑accounting workflow.

¶ 10. Summary

The Journal Entry feature provides a structured, compliant method for recording manual adjustments in the general ledger. With support for debit/credit lines, account selection, descriptions, and full audit trail tracking, it ensures accurate financial reporting and supports accountants in maintaining clean, compliant books.